The Rocky Mountain Institute’s Business Renewables Centre (BRC) have recently launched a new mapping tool aimed at helping large-scale buyers and developers of renewable energy better understand market economics and price trends by location. By utilising this software platform, companies will be able to identify which wholesale power markets across the U.S. provide the best market for utility-scale renewable projects.

The new mapping tool can identify locations across the US that are good sites for wind and solar farm development, show areas in the southeast and parts of the western US where there is currently no access to open markets for non-utility buyers and can also demonstrate how the value of a wind or solar farm can vary even within a state, such as Oklahoma, while also highlighting areas of congestion.

BRC’s Mark Porter and Josh Constanti shared their Skype screens with me online to walk me through a demonstration model of the platform and show how it all works.

Hi Mark and Josh, to start off with, can you give me a background of yourselves and a general background of what RMI and the Business Renewables Centre is up to at the moment, generally?

Mark: The Business Renewables Centre is a programme under the Rocky Mountain Institute. We were formed in August 2014 to help enable renewable energy transactions with non-utility buyers. To date, the majority of transaction have been with corporate counterparts, but we have a community of 210 members and within that there are a number of municipalities and universities, schools and hospitals. So not all corporations. We have built up a community with buyers and sellers, i.e. renewable energy project developers and service providers in the community.

To understand the needs of the market, we bring our membership together every six months and after a very limited time in plenary ask attendees to vote with their feet and select workshops, and subsequently into greater detail at table-level discussions. Each of the workshops and table discussions represent a barrier or challenge. An attendee will look at the list and decide where to go: to learn something, and/or to impart experience and add value, to teach. Each attendee can select two workshops and two table-level discussions to attend. At the end of day 1 we ask people to vote on what they feel are the biggest barriers. From a room of four hundred people the voting usually highlights 5-6 issues from a list of 20. These 5-6 top issues roll forward to the next day, which is spent on solutions. The solutions sessions drive the tools and resources the BRC team need to develop over the proceeding 6 months.

We always work with members, so whenever we’re developing anything new, we always have a task force of members with experience, or interest finding solutions to the problem right now, or have overcome the challenge somehow and are seeking to codify the practice, allowing others to follow in their footsteps a little bit quicker, easier and more effectively.

With regard this new tool, what you’re looking at on the screen are three areas of our online resources, the results of six or seven different gatherings we’ve had.

The ‘Learn’ section [the left hand image in the image above] is effectively a library. We have primers and guides on very specific topics, template and articles covering specific subjects.

Imagine people are voting and so bubbling up to the top is ‘The Need To Understand Risk’, “how do I allocate risk when I am discussing a power purchase agreement?”, or accounting – “How do I work with my accounting team to align PPA-terms with our accounting policies?”. So these are very specific primers and guides on those specific areas. These sorts of things are usually about 50-60 pages long, covering the full gamut of issues on that specific topic. Other things like templates and articles are stored in the library as well. This library is for members to access whenever they need.

The next area of resource is designed to help buyers find opportunities in the marketplace. There are about 23 GW of projects on this platform and most easily described as an estate agent with houses. Developers post up their projects and select which can be seen by buyers. We limit the number of projects visible to buyers (at any one time) as a way of quality control, self-selection, so they can pick the best projects. Developers can see their own projects, while buyers can see all projects from our 55 developer members. Buyers can search for projects using filters, look at specific projects, access contact details, see where the project is, the level of development and who is the developer. Buyers can also make requests. Buyers first review what developer-members are offering them, and can make a specific request. They can ask “specifically I am after a project with x, y and z characteristics. What have you got?” They can also see profile pages covering the developers we have in our community.

Moving on, for context, we found, especially in 2014 and 2015, that buyers completed transactions and subsequently wholesale power prices have fallen. Most of the purchases have been using a virtual power purchase agreement structure, which is akin to a hedge on electricity prices. Given the fact that the wholesale base cost has fallen, some of those hedges are now out of the money. We’ve spoken to all the buyers in our membership, we’ve asked them whether they have any issues with this. They said no and that that they went into this with their eyes wide open, knowing this could happen.

However, what is happening is that many other buyers, newer buyers, coming into the marketplace have read the reports and are concerned. Our perspective from the point of view of the Business Renewables Centre is that these concerns are valid, and we would always advocate really understanding the risks involved, that said, ultimately it’s a hedge. Historically you can’t really hedge electricity, you can’t really buy a long-term contract for electricity without paying through the nose for it. Typically, most tariffs or rates last for two, maybe three years at most. So, the contracts that a lot of these non-utility buyers have been purchasing for 10, 12, 15 years and upwards are effectively a long-term hedge on electricity prices. These power purchase agreements, for the buyer, mean they are paying a fixed rate of electricity.

People typically don’t sign hedges to make money. They are seeking a period of stable business planning. For example, if currency swings have a material impact on a business, a currency hedge might be a useful tool to manage revenues and build in some consistency to allow planning. These contracts are no different.

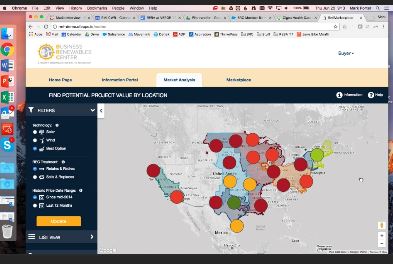

We’ve developed this tool for a number of reasons. Firstly, to help buyers think about economics. No-one’s going to make an investment based on this tool, but the tool is to encourage and support buyers to think about the economics around these projects, which they do, but we want to make sure that project-location is included in that analysis. Project location is a key factor, so we thought it was important to help buyers understand how location can impact the economics. We also thought it was important to help developers understand the new wave of customers. The existing development model has been to develop projects for utility counterparts, which are a very different customer to the commercial, industrial or institutional buyer. The established approach to project development has been essentially to find the area of highest resource, with a cheap grid connection and build at the lowest cost. This doesn’t always work if you are a non-utility buyer, as the non-utility buyer also needs to consider the market value of electricity.

So, this model is comparing the average cost of electricity from the local node, which is a pricing point on the grid, to the levelised cost of wind and solar. If the price from the node is, say, $100 per MWh, the levelised cost is $80 per MWh, the buyer and seller (project developer) are able to negotiate with a $20 per MWh margin, call this room to manoeuvre and to negotiate around. If the buyer wants more risk protection in a certain area, there will be a cost, but with the room to negotiate allows this. If, however, you have a cost of generation, a levelised cost of energy of, say, $15 per MWh, a buyer might think that’s wonderfully cheap. However, if the cost of electricity from the local node is $10 per MWh, then that project is technically losing money, $5 per MWh, every MWh, so the contract has to be at $15, if not above that. The same situation regarding term negotiations doesn’t start on the same footing because the developer has already had to adjust the PPA rate above the local cost of electricity, which the buyer is paying, just to cover costs.

This tool doesn’t take into account time of day pricing, or local state policies. it’s more of an average. In reality, when considering a transaction we need to consider the time of day when buying electricity, compared to when is the project generating. A timing mismatch could end up costing the buyer more.

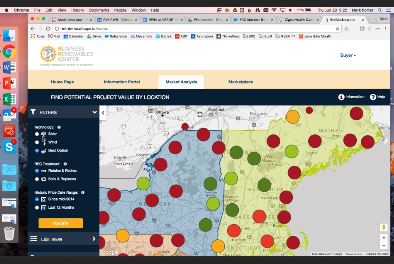

The way the tool works is that all these coloured areas are the deregulated wholesale markets in the US. Those areas are where you can easily undertake a transaction. The grey areas are regulated areas, where it is not impossible to do transactions, however transactions need to be sleeved through a utility if it is possible at all. There isn’t much publicly available data as to what the price of electricity actually is in those regions, and therefore makes analysis very difficult.

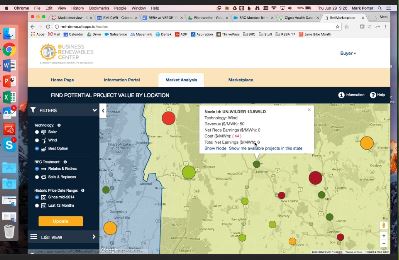

There’s about 4,300 nodes across the US that we have data for. As an example, the screen is showing me that Vermont, New Hampshire and western Massachusetts could be good areas to investigate further. I can zoom down to a single node, and see that a wind project earns on average $50 per MWh, the levelised cost of wind is $44 per MWh, providing a positive delta of $6. Under this scenario the buyer is going to retain and retire the RECs, and the average electricity cost is based on the last three years’ worth of data.

If I click on a node, the tool takes me to the model results behind it, such as what it is, what are my calculations for wind and solar, model assumptions, how the calculations stack up for both wind and solar technologies.

Then it’s a question of what projects are available in the area? The model links to the Marketplace we saw earlier, and show any available projects. Alternatively, the buyer could make a request to developers “I am looking for something in New Hampshire, what have you got?”

BRC membership for buyers comes at no cost to join and access education. In addition we have a series of bootcamps, which are essentially training sessions, allowing buyers to learn, with experienced buyers present as faculty, and understand what are the issues, what are the risks, so that buyers can be aware, before actually go into doing a transaction they have already effectively walked through the process in a training environment.

Josh: The developers, we’ve often noticed, concentrate on cost, almost solely on cost. From a buyer’s perspective, that’s not the full consideration. This tool shows you can have a region that is windy, will be better financially, from a buyers perspective, wholesale prices will be much higher than an area like Oklahoma that’s been flooded with resources that have now driven the price down. So, it’s also the goal of the tool that developers think a little bit differently when it comes to non-utility buyers.

Mark: It’s helping developers to understand that this new customer base, are not utilities, and have different criteria.

How does this compare with other tools, and advance the software that’s out there?

There’s nothing out there that we know of that does this. There are other mapping tools, but to our understanding, there is nothing else that does this, specifically for non-utility buyers when they are interested in contracting with the renewable energy projects directly, there’s nothing else out there that would come close to this.

How did you put this tool together?

We started off by doing a lot of work to get hold of the raw, underlying price data. That was the big trick. You can imagine that each individual grid-area has a different set of requirements, price data is stored in a certain way, each grid-region compiles the data differently. So getting access to data was the biggest challenge we had. Then, harmonising that data so that it’s all in one consistent format was the next, pretty large, challenge. The subsequent challenge, on an ongoing basis, is that periodically, for no known reason, one of the regions will decide it needs to change everything completely. So all the formatting that we had previously done has to be remapped and re-updated. So data gathering has been the biggest challenge.

What is the overall span of people who could be using this, besides developers and buyers?

All across our membership base, so 110+ buyers of various different stripes, so that would be the large IT companies, some heavy industrials, schools and hospitals, a lot of Fortune 500 entities in there, groups who are consultants themselves, brokers, lawyers and accountants, we have a couple of equipment manufacturers in there, etc etc. The last sub-category within our service providers, so users would include specialist power market experts, people who do balancing and scheduling or who work on dispatch, etc.

Is this just a model we’re looking at or is this up and running now?

It is very much up and running and people are using it and coming up with any questions they have. We have a 7-8 page ‘How to Use This’ guide that each user has to go through so that they understand how it actually works. We keep it behind a member firewall, it’s better that way because if there is anything out there that is a little more sensitive, at least they know it’s restricted. That said, with 200 members or so it’s not that restricted, but it’s not completely out in the public domain.

Potentially, could there be versions of this for use with markets outside the US, or is it just the US at the moment?

Right now it’s just the US and that’s really because of the data. The model does what it does, so provided we can access the nodal data and understand what the levelised cost is in that region, in the UK or in Europe, we could do this. We built this platform to be global.

Images: Screenshots from the Skype interview of some of the screens of the new mapping tool (Copyright: Rocky Mountain Institute).

For additional information:

Business Renewables Centre (Rocky Mountain Institute)