The PUN price of the Italian electricity market IPEX rose the first 11 months of 2018, 8.01 €/MWh compared to the average of the first eleven months of 2017. According to the analysis carried out by AleaSoft, this price increase has been caused by the increase of the fuels price and CO2 emission rights price, which particularly affect Italy where a high percentage of the demand is covered by thermal production. In the first eleven months of 2018, the Italian market has positioned itself as the second highest price among the main European electricity markets behind the British N2EX market.

In the IPEX market, year-on-year increases have been recorded in all months of this year, except in January, due to the fact that in January 2017 the Italian market was affected by the French nuclear shutdowns. The average PUN price of each month of 2018, except for January, has been higher than the average price of the last five years for the corresponding month.

In 2018 the geographical area with the highest price was Sicily.

Until November of this year, the Italian electricity demand had increased 2.2 percent compared to the same months of 2017. In the first quarter of the year the average temperature in Italy was similar to that of the first quarter of 2017 and in the rest of the year it has been slightly higher than the previous year.

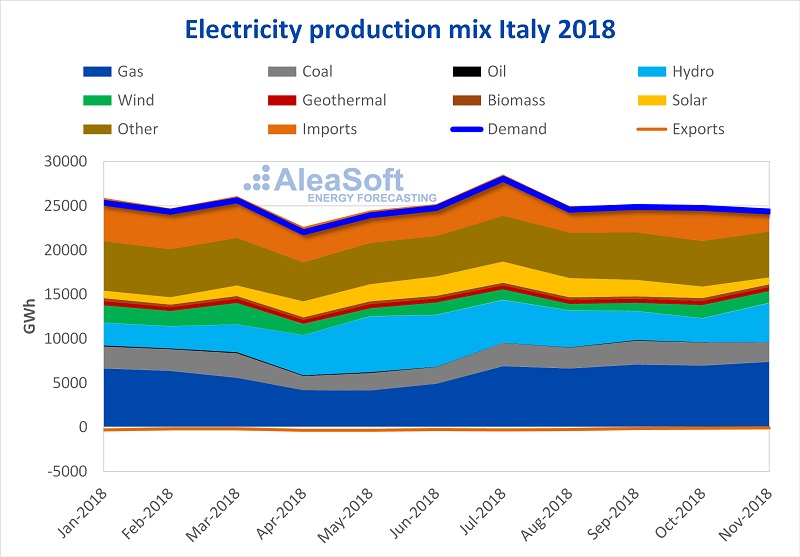

As analyzed by AleaSoft, although thermal production in 2018 decreased by 5.5 percent compared to 2017, if the first eleven months of the year are analyzed, 55.9 percent of demand was covered with this type of technology. During the first eleven months of the year the production of electricity using gas was the highest, covering 24.5 percent of the demand, followed by production with other thermal technologies, with a 20.4 percent share, while the production with coal occupies the fourth place with a 9.3 percent share.

On the other hand, production with renewable technologies has increased by 13.4 percent over 2017. This is mainly due to the hydroelectric production increase of 34.4 percent during this period, standing as the third largest production technology in Italy during the first eleven months of the year. In the analyzed period, wind energy increased 1.1 percent and solar energy decreased 9.3 percent over 2017.

The fact that Italy's demand is covered in a high percentage with thermal production means the price of the Italian electricity market is heavily influenced by the price of fuel and the CO2 emission rights and this year there has been a generalized increase in them. If one compares the average price of fuel and CO2 emission rights in the first eleven months of 2018, with the average price of 2017 the following data is obtained: Brent has risen 18.06 $/bbl, gas, 5.35 €/MWh, coal, 8.95 $/t and CO2, 9.45 €/t.

Sources: Prepared by AleaSoft with data from TERNA and ENTSOE.

GME (Gestore dei Mercati Energetici) is the Italian electricity market operator. It also operates the gas and environmental markets. IPEX (Italian Power Exchange) is Italy's wholesale electricity market. Related to electricity, GME operates:

Terna is the operator of the Italian electricity system and is in charge of high voltage electricity transmission networks throughout the country. Terna is in charge of the auxiliary services market MSD (Mercato del servizio di dispacciamento).

Italy's electricity system is divided into zones. A zone is a part of the electricity network where physical limits exist for the transfers of electricity to/from other geographical areas for reasons of system security. The zones are classified into geographical zones, national virtual zones and foreign virtual zones. The geographical zones represent a part of the national network; there are currently six active zones: Northern Italy (NORD), Central-Northern Italy (CNOR), Central-Southern Italy (CSUD), Southern Italy (SUD), Sicily (SICI) and Sardinia (SARD). National virtual zones represent a set of generating units connected to a part of the transmission network, whose maximum exportable generation to the rest of the grid is less than the maximum possible generation due to insufficient transmission capacity; currently there are the following: Brindisi (BRNN), Foggia (FOGN), Monfalcone (MFTV), Priolo G. (PRGP) and Rossano (ROSN). Foreign virtual zones: are the points of interconnection with neighbouring foreign countries; they include Austria, Slovenia, Corsica, France, Greece, Switzerland and Malta.

The market zones are built by the aggregation of geographical and/or virtual zones, so that the flows between them are lower than the limits of transmission notified by Terna. This aggregation is defined per hour as a result of the resolution of the daily and intra-day markets.

Macro-Zones are the aggregation of geographic and/or virtual zones defined for the preparation of statistical market indexes. A Macro-Zone has a very low frequency of market splitting in addition to a similar trend in market prices. Since January 1, 2009 the Macro-Zones are the following: MzNord (includes the northern and Monfalcone areas), MzSicilia (includes the Sicily and Priolo areas), MzSardegna (includes the Sardinia area) and MzSud (includes the remaining areas).

In the daily market the trading of purchase and sale offers for each hour of the following day is carried out.

The daily market MGP is a marginal market in which the price and volume of each hour are established from the point of equilibrium between supply and demand. All matched sales offers and matched purchase offers related to pumping units and consumer units that belong to foreign virtual zones are valued at the marginal price of the area to which they belong. Matched purchase offers referring to units of consumption belonging to Italian geographical areas are valued at the single national price PUN (Prezzo Unico Nazionale). The PUN price is equal to the average of the prices of the zones, weighted by the quantities purchased in these zones.

In the intra-day market electricity purchase and sale offers are traded for each hour of the next day, which modify the program resulting from the daily MGP market. The intra-day market is also marginal. Unlike the daily market, all matched offers, both purchase and sale, are valued at the settlement price of the area. The intra-day market takes place in seven sessions: MI1, MI2, MI3, MI4, MI5, MI6 and MI7.

Italy will begin to participate in the European XBID intra-day market from the second start-up of it, which is scheduled for 2019, in spring or early summer.

Guarantees of Origin (GO) are assigned to electricity producers from renewable sources that generate and inject electricity into the grid each year. Its objective is to promote transparency in contracts for the sale of renewable energy. In Italy, GSE (Gestore Servici Energetici) is responsible for issuing guarantees of origin to plants that generate electricity from renewable sources.

Contracts for the sale of renewable electricity to final customers must be certified by a series of guarantees equal to the amount of electricity sold as renewable under the same contract. To this end, each selling company must obtain a quantity of guarantees of origin equal to the electricity sold as renewable. Each guarantee of origin equals 1 MWh. Guarantees of origin are issued from the following sources of renewable energy: hydroelectric, wind, solar, geothermal and others.

Guarantees of Origin are negotiable certificates that can be sold or bought in the market of Guarantees of Origin M-GO, organized and managed by GME, or through bilateral contracts. M-GO market sessions are normally held monthly, and use the continuous market mechanism. On the other hand, GSE organizes periodic auctions of guarantees, at least quarterly.

In 2018, the price of Guarantees of Origin in the M-GO market has tripled, and in some cases quadrupled, with respect to 2017. In 2018 the price of Guarantees of Origin has been above 1.19 €/MWh when in 2017 it was above 0.30 €/MWh.

The fact that Italy has so much thermal production and that it does not have nuclear production implies that the challenge of reducing CO2 emissions will be greater.

In Italy the solar resource is high. It is estimated that in the southern part of the country there are more than 2000 hours of sunshine per year. According to data published by ENTSOE (European Network of Transmission System Operators for Electricity), solar power installed in Italy in 2018 is 4.7 GW, and according to the TYNDP (Ten-Year Network Development Plan), also of ENTSOE, in 2040 solar power can be higher than 58 GW, and even 117 GW according to the most optimistic scenarios. According to AleaSoft, an increase in solar installed power in Italy can bring the price of the IPEX market closer to that of other European countries.